© All content copyright NBR. Do not reproduce in any form without permission, even if you have a paid subscription.

An Australian fund with $A5 billion under management says it might sell its Chorus shares if the government lets a Commerce Commission ruling to slash copper line pricing stand.

“We’d have to reconsider our investment, of course,” Investors Mutual Limited (IML) senior portfolio manager Simon Conn tells NBR.

The government has called in Ernst & Young Australia to review Chorus’ finances, and its capability to rollout the Ultrafast Broadband (UFB) fibre project, in the wake of the Commerce Commission’s determination to cut Chorus’ copper line pricing by 23%.

Mr Conn, who frequently appears in the Australian business press, tells NBR that IML will not be making further investments in NZ companies in regulated sectors until the Chorus situation is clarified.

IML’s stake in Chorus [NZX: CNU] is below the 5% threshold, but Mr Conn says it holds “a few million” in the company’s shares.

In a letter to Prime Minister John Key (see RAW DATA below), the portfolio manager says IML is a long term “substantial” investor in Sky City. It also has holdings in Mighty River Power, Fletcher Building and Z Energy.

Mr Conn says IML favours long-term, infrastructure plays.

As such, Chorus dividend policy, which saw $95 million returned to shareholders last year, is one of the attractions for the fund.

He notes that last year, “Chorus earned profit of 44c per share and paid a dividend of 25.5c per share, a seemingly conservative payout ratio of 57%.”

Mr Conn sees that payout ratio as sensible; enough to attract new investors, but still leaving enough profit to fund Chorus leg of the UFB rollout (Chorus is responsible for around 70% of the UFB rollout by premise).

While he was heartened by Mr Key’s initial staunch defence of Chorus, he’s concerned about more recent, ambivalent statements from the PM and ICT Minister Amy Adams.

So are analyst, to a degree. Forsyth Barr’s Drew Galpin sees a possible deal with the government that would see the copper price cut over-ruled, but Chorus’ dividend halved to appease the company’s industry foes.

A lobby group called the Coalition for Fair Internet Pricing, which includes Consumer, InternetNZ, Tuanz, and ISPs Orcon and CallPlus (supported at a distance by Vodafone), has argued that if the government’s counter-proposal for much more modest copper price cuts goes through, the money otherwise lost to Chorus would go into shareholders’ pockets as dividends rather than subsidise the fibre rollout.

The Coalition says the government must allow the Commerce Commission cuts to stand. It says the regulator was following the Telecommunications Act (2010); that its cuts followed a straight-down-the-line process of international benchmarking. Fibre should be made more attractive in terms of pricing, speed and opening up content competition, it says [UPDATE: the Coalition has fired off an attack on Mr Conn; read it here.]

Chorus says the cuts would blow a $1 billion hole in its earnings, and inhibit its ability to borrow to complete the remainder of the UFB. The company recently suspended dividend guidance while the EY review is under way.

For Mr Conn, the situation is clear cut. He says John Key and Amy Adams were correct to say the Commission made a mistake, and too narrowly interpreted the Telecommunications Act.

Like others in the Chorus camp, the fund manager is perturbed that the government did not immediately make good on its threat to over-rule the regulator after the Commerce Commission made its final price determination on October 31, but rather started to equivocate, calling in EY.

ForBarr’s Mr Galpin (who has a buy rating on Chorus). Is optimistic long term. He says the government is merely leaving a diplomatic pause, not wanting to be seen to be “simply handing money to Chorus.” When the dust settles, it will still back the company. (And NBR notes the government and Chorus’ fates are intertwined;the Crown is in the process of investing $929 million, half in non-voting shares, half in interest-free debt securities). Mr Galpin says while the dividend could get crimped, but it be only for 24 months. Medium to long term, he sees no way the government would put Chorus, and by extension its showpony UFB programme, at risk.

But others, like Craigs’ Mr Dekker (who has a hold rating on Chorus) are more pessimistic on dividend and earnings prospects.

Mr Conn is simply frustrated at the reviews, the political arm wrestling, and the potential changing of the rules.

The fund manager says the Telecommunications Act (2010) allows for what he calls a “good and innovative” fibre rollout model that is more cost-effective than the equivalent project across the Tasman. Cashflow from copper can fund the fibre rollout (the Coalition says the Act’s provision for a move from retail-minus to cost-plus pricing was always going to involve a steep copper price cut).

But he sees the Commerce Commission undermining the Act at every turn.

In particular, Mr Conn seizes on Ms Adams’ line that copper pricing should reflect the price of a replacement network (that is, the UFB fibre rollout underway). But he says it makes no sense that the Commerce Commission puts a regulatory value of $1.6 billion on Chorus’ leg of the UFB, while Vector’s power line network, which reaches 28% of the population, is as a regulatory value of $2.5 billion.

“The election of the Key I thought heralded the return of sensible government where investments are not subject to adverse regulation and the rule of law is upheld,” he says.

The Commerce Commission has clearly not followed the Act, in his opinion, and he can’t see why the government has not moved immediately to over-ride the regulator, rather than hiring EY.

“The stable regulatory environment has always been a good reason to invest in New Zealand,” he says.

“But this decision makes me question that,” he tells NBR.

If the Commission’s decision is allowed to stand, cheaper copper broadband will give consumers no incentive to switch to fibre, and the UFB will become “a white elephant Chorus is forced to build.”

The ability of all NZ regulated utilities to raise equity and debt will be compromised, he says.

ABOVE: The graphic that accompanied Mr Conn's letter. Click to zoom. (NBR would note costs are a moving target. In February, Chorus raised its initial estimate of UFB costs by $300 million to between $1.7 billion and $1.9 billion.)

RAW DATA: IML senior portfolio manager Simon Conn's letter to Prime Minister John Key

(It was sent November 19. As of last night, Mr Conn said he has yet to receive a response from the PM, or any of those CC'd, who included ICT Minister Amy Adams, Treasury Secretary Gabriel Makhouf and vaious MBIE officials - CK.)

From a deeply concerned Chorus shareholder

Dear Mr Prime Minister

IML is a Sydney based Fund Manager with AUD$5bn under management on behalf of retail and institutional investors. We are long term investors in the companies we own and have been investors in several NZ companies for many years (for example Sky City (in which we are a substantial shareholder), Fletcher Building, Chorus and more recently Mighty River Power and Z Energy). We are supportive shareholders of the companies we invest in and believe we represent the sort of patient capital New Zealand companies seek to attract to their register.

Our investment process involves buying and holding companies which generate sustainable and recurring cashflows from which they can pay a sustainable and growing dividend over time. It is our experience that a significant part of the return an investor receives from investing in a company is from the dividend it pays.

IML has a long history of investing in infrastructure assets and are currently shareholders in several such companies. The concept of earning a reasonable return (as determined independently by a regulator using a well established set of rules) on an infrastructure asset is well understood by capital markets. This model has long been supported by debt and equity markets and has allowed many Australian and New Zealand companies to raise significant amounts of capital over a long period of time to invest in essential infrastructure on both sides of the Tasman, to the benefit of consumers and businesses alike.

We are currently shareholders in Chorus, having been initially attracted to the highly recurrent cashflows the company generates from its ownership of the copper phone network in NZ. It was our view on investing that this cashflow would enable Chorus to pay a regular and consistent dividend to shareholders whilst at the same time constructing the new fibre network for NZ, the so-called “UFB network”. In fiscal year 2013, Chorus earned profit of 44c per share and paid a dividend of 25.5c per share, a seemingly conservative payout ratio of 57% of earnings. It is our understanding that this dividend policy was established by the Chorus board to ensure that sufficient retained earnings would be available to complete the UFB construction, whilst maintaining an investment grade credit rating. This policy seemed to us prudent, reasonable and broadly in line with other regulated utilities and as such sustainable. It is on this basis that we invested in Chorus.

However, we are completely at a loss to understand how the recent regulatory decision which has led to the regulator proposing to cut the UBA price by almost 50% has been arrived at and how the government can let this decision stand. We do not understand how a regulator can set the price for accessing a copper network in New Zealand by reference to copper networks in Denmark and Sweden. Surely this is a complete misreading of the legislation that governs this area and is at odds with the intention of the legislature. It certainly flies in the face of common sense and contradicts everything that was understood (including by equity investors and Chorus management) when Chorus was created.

On reading the legislation this decision seems perverse. The legislation requires the regulator to set the price for accessing copper by reference to the replacement cost of the asset. As Ian Martin from CIMB has opined the tenders received in NZ recently for the construction of the NZ UFB, which was a competitive process, should have given the regulator an insight into what an infrastructure owner would have to spend to build such a replacement network in New Zealand. NZ is a country with challenging topography and has many other differences to countries such as Sweden and Denmark, which make a nonsense of setting the price for accessing Copper in NZ by reference to these other countries.

This regulatory decision also places Chorus in an very difficult position at just the point in time when they should be entirely focused on building the UFB network, which is an important piece of infrastructure for New Zealand’s future. The entire premise on which Chorus was created is based on the fact that they would be able to charge a reasonable price for access to the copper network and utilize the cashflows that this generates to fund the rollout of the UFB, whilst also servicing their non-Crown debt and paying a reasonable level of dividend to their shareholders. As we have stated this is the entire basis by which every other regulated utility in Australia and New Zealand operates.

We are also concerned that the Copper network itself requires significant investment to maintain it in a fit and proper state, being the backbone of NZ’s communications infrastructure. This decision may also impact the ability of Chorus to maintain this asset by reducing cashflows at a point where Chorus is committing significant resources to the UFB.

The rate charged for access to the Copper network, it was well understood at the time of demerger, was not set in isolation. Consumers and businesses can either pay to use the copper network or in future can switch to using the new UFB network once it is rolled out past their premise. If the copper price is allowed to stand at $34.44 and with fibre prices starting at $37.50, there is no incentive for users to switch to fibre and the UFB becomes completely uncompetitive. With the government having mandated that NZ have a 20% usage of the UFB by 2020, Chorus shareholders now face the real risk they will be levied with penalties. This could happen despite Chorus completing construction of the UFB on budget and on time.

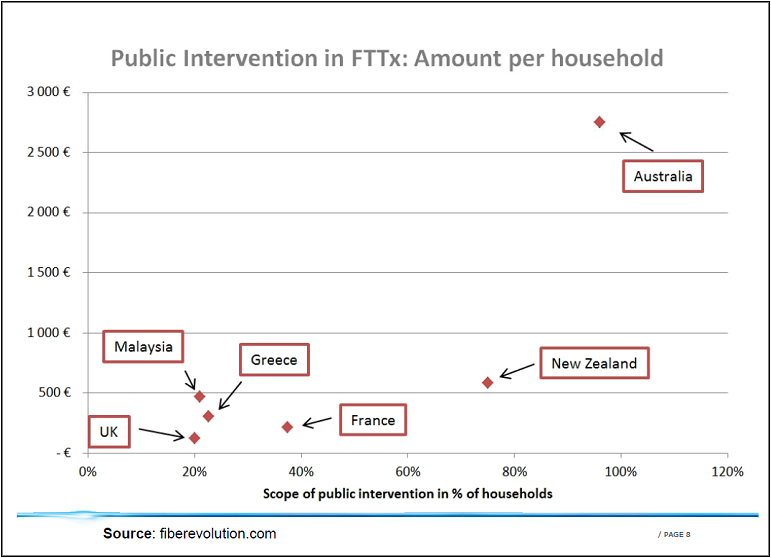

We believe Chorus management are doing an excellent job of managing the rollout of the UFB and believe the model created by the NZ govt is far superior to the Australian model, for example. This was highlighted at the companies recent AGM (see the chart presented at the AGM below ). Chorus as owner and operator of the copper network are the logical and appropriate party to manage a significant part of the construction of the UFB network.

We note with concern that Moodys have downgraded Chorus’s debt rating and that yesterday the company has publicly stated that they are withdrawing their previous dividend guidance. We also have heard there are concerns that the company may have to raise equity all because of this adverse regulatory outcome. To facilitate this large capital expenditure programme Chorus needs access to funding, that funding must come from the cashflows derived from the copper network. The government should be aware that shareholders have no appetite to fund an equity raising at this time. Why should shareholders be called on to build what will quickly become a white elephant!

If the government is not willing to intervene to address this failure in the regulatory price setting process then we will be calling on Chorus to do everything in their power to slow and eventually end their expenditure on the UFB. Why construct a network for which there will be limited take-up?

This decision, if allowed to stand, has broader implications and we believe will undermine the entire regulatory price setting process in New Zealand no doubt impacting the ability for all New Zealand regulated utilities to raise debt and equity. We believe it has already had an impact on the standing of New Zealand in the international investment community at just the point in time when New Zealand is seeking to raise significant funds from overseas investors. We note a recent research piece by Greg Main of First NZ Capital where he compared the copper network of Chorus to that operated by Vector, the NZ regulated electricity utility. In this note (copy attached) he observed that the Vector network which covers only 28% of the NZ population and runs for 18,000 km has an implied regulatory value of $2.5bn. By comparison, the regulatory value of the Chorus copper network implied by the recent decision by the Commerce Commission is only $1.6bn – this is for an asset that spans the entire country and has some 130,000km of copper and 30,000 km of fibre. What are Vector’s shareholders to think if this decision is allowed to stand?

Chris Keall

Tue, 26 Nov 2013

Tue, 26 Nov 2013

© All content copyright NBR. Do not reproduce in any form without permission, even if you have a paid subscription.

Free News Alerts

Sign up to get the latest stories and insights delivered to your inbox – free, every day.

Free News Alerts

Sign up to get the latest stories and insights delivered to your inbox – free, every day.

Chorus: $A5b Aussie fund manager puts govt on notice

34049