On offer: an alternative to the 1-3% inflation MPR range and 2% target.

The RBNZ has had a 30-year international reputation for being the world’s best little central bank and built this reputation on the back of the 1990 version of the Monetary Policy Committee Remit. Is this remit still fit for purpose? Is it nimble enough to get New Zealand through these exceptional times?

I remember clients lining up to hear Don Brash speak in London in 1991. The RBNZ has been historically lauded for its courage in experimenting with different monetary policy tools and measures in seeking to achieve its mandated objective of maintaining price stability, initially through a Policy Targets Agreement (PTA), and latterly a Monetary Policy Committee Remit with the New Zealand Minister of Finance.

In 1990, the PTA began as a mandate to contain inflation between 0-2% (under Don Brash) until 1996, when it was widened to 0-3% (still Don Brash). In 2002 it changed to 1-3% with a mid-point target of 2% (Alan Bollard) and has remained in place, albeit employment was added to the remit in 2018 as an amended dual mandate (Adrian Orr). The current Monetary Policy Committee Remit requires the RBNZ to keep inflation between 1% and 3% on average over the medium term, with a focus on keeping future average inflation near the 2% target midpoint and supporting maximum sustainable employment.

In essence, a rules-based mandate has now had a more social KPI thrown into the mix.

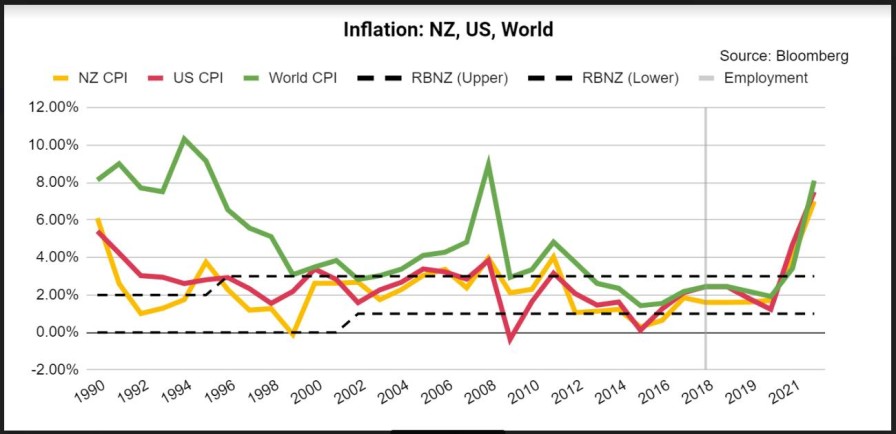

Looking at the timeline below, it is not a coincidence that the original PTA was implemented and further amended following significant spikes to US and global inflation.

Caught global attention

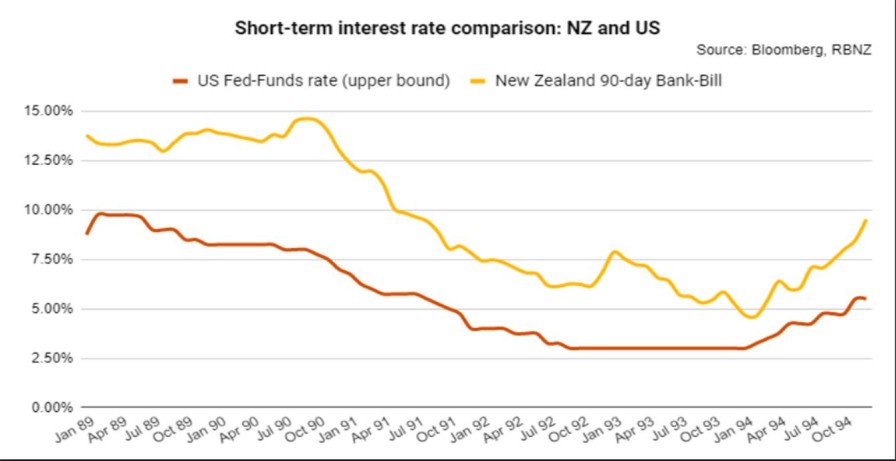

As can be seen above, when US inflation is above 3% New Zealand inflation tends to follow. The exception was in 1990 following the implementation of the PTA, where the RBNZ kept interest rates higher for longer (above 12.5%) and forced a rapid decline in New Zealand’s inflation rate.

It was this RBNZ activity that caught the attention of global central banks and many followed suit with negotiated independence and similar targets.

In August 2022, at the Jackson Hole Symposium, US Federal Reserve Bank chair Jerome Powell commented that, historically, the Fed had taken its foot off inflation’s throat during the late 1980s and early 90s and paid the price, warning the market it would not make the same mistake again. This is nicely illustrated in the following chart.

It is not an easy journey for New Zealand as a small, geographically isolated, and dynamic trading economy, significantly affected by global economic and financial market influencers such as inflation, interest rates, commodity prices, and currency values. We survive off trade and, accordingly, we have a competitive dependency on our trading partners.

Should a small (five million population) and relatively volatile economy such as New Zealand be handcuffed in its ability to nimbly bend with inflation impactors outside its control?

Inflation tracker.

A rigid 3% inflation cap appears somewhat arbitrarily oppressive, given most inflation impactors are of global origin, ie, not directly within the confines and control of New Zealand’s domestic economy.

What is so magical about 3% as an inflation cap if most of New Zealand’s trade partners are exceeding it?

Most other global central banks also have a rigid 3% cap on their respective inflation target ranges and, currently, 17 of the world’s top 20 economies have inflation higher than 5%. These are exceptional times, not seen since the late 80s and early 90s, a time when the world’s leading economies were significantly less leveraged with debt than they are at present.

Should a more dynamic and socially elastic alternative monetary policy remit be considered as a default mechanism during times of global stress when global supply constraints are powering global inflation rather than more localised demand issues?

The default Monetary Policy Remit alternative

I am not suggesting we necessarily toss out the current range and target; instead, redefine the current 1-3% range and target of 2% as a “stretch target” during times of global inflation stress (using US inflation > 5% as the proxy).

During these ‘global stress’ periods, our monetary policy remit defaults to a simple comparative that keeps New Zealand within an acceptable inflation boundary of our major trading partners.

This allows New Zealand to remain internationally competitive in the all-important trade component of our economy.

New default formula: New Zealand Inflation is not to exceed the weighted average inflation rate of New Zealand’s top 10 trade partners/trade blocs.

The 10 trade partners in the table represent circa 80% of New Zealand’s trade.

Accordingly, under the default mechanism, the RBNZ would need to ensure that New Zealand inflation does not exceed 4.33% and not bust a gut to achieve an inflexibly ruled cap of 3%.

When the US inflation proxy of 5% is no longer triggered, the target resets to 0-3% with a mid-point of 2%.

The higher cap avoids the RBNZ unduly straining New Zealand’s social fabric with punishing high interest rates and unduly haemorrhaging GDP growth continuity.

The focus is instead towards measurable trade competitiveness. This could also reduce the current sponginess of the RBNZ’s monetary policy brakes and accelerator, especially if real time data helps influence the timing of such actions, ie, act dynamically rather than through a rear vision mirror with a concave view. (I refer to the recent exciting launch of the worlds’ first real time country inflation tracker on GDPlive.net).

A significant difference between global (and New Zealand) inflation of the late 80s, early 90s is that economies are now highly leveraged in terms of government and household fiscal debt, both on and off-balance sheet.

Economies are far less resilient to high interest rates.

New Zealand’s trade-based economy is predominantly supported by SME’s that are increasingly needing to fund supply chain-affected timing differences with bank-sourced working capital. High interest rates will negatively affect sustainable productivity for our trade sector, and having a central bank playing strictly by an arbitrary rule book is not conducive to “all-weather monetary policy nimbleness”.

Stuart Henderson.

Inflation tracker

The recently launched Inflation Tracker – alongside the world’s only country GDP live tracker – also has a neat tool called Optimal OCR. This tracks where the OCR should be currently set if using a strict Taylor rule based 2% mid-point monetary policy target.

It is currently 8.40% suggesting the RBNZ is currently 4.10% too low in where the OCR should be if playing by the strict ‘Taylor’ rules.

By moving the 2% monetary policy target to the above trade weighted rate of 4.3%, the gap closes significantly, thereby giving the RBNZ some much needed breathing room.

The new default mechanism also, arguably, focuses monetary policy actions to more closely align productivity efficiency.

Efficient and sustainable productivity encourages better and more consistent social outcomes in higher wages, higher employment rates, and intergenerational international competitiveness and reduces the risk of RBNZ actions being too slow, too late, too little and too much (so long as the RBNZ start utilising real-time data).

Is the current remit nimble enough? No, I don’t believe so.

Can we customise the remit to be more Kiwicentric and nimble? Yes, a link to our trade partners gives us this flexibility.

The default remit should provide better scope of certainty for New Zealand society in terms of forward planning around debt/interest rates and trade. It modernises an outdated rule system built for a different world.

Stuart Henderson is an independent financial market risk adviser with more than 35 years’ experience, including as a partner at PwC.