OPINION: Why I won't be investing in Facebook

Lance Wiggs digs behind the IPO statement's headline numbers. Be warned.

Lance Wiggs digs behind the IPO statement's headline numbers. Be warned.

Facebook’s daily user growth is slowing. While 6-10% growth per quarter feels like a lot when annualized, it is getting close to being a normal company.

The social network is running out of target market, and especially target market with pockets deep enough to be monetised.

The monthly active user chart is falling harder, and explains why I keep getting those annoying “Lance, you have notifications pending” emails. They are trying hard to keep these numbers afloat.

(Click any graph to enlarge)

The Summary Risk Factors deserves reading and thought (read Facebook's full SEC filing here). Be warned.

If we fail to retain existing users or add new users, or if our users decrease their level of engagement with Facebook, our revenue, financial results, and business may be significantly harmed;

Related to this is the boilerplate: Our business is highly competitive, and competition presents an ongoing threat to the success of our business;

This is the principal risk. If users migrate to Twitter and other platforms as Facebook follows in the footsteps of MySpace, Friendster and Bebo into uncool obscurity then the house of cards falls apart. Nobody can say what users will do, but the charts above should be the most closely watched, as well as the amount of time users are engaging.

We generate a substantial majority of our revenue from advertising. The loss of advertisers, or reduction in spending by advertisers with Facebook, could seriously harm our business;

This is the second biggest risk, though I would characterize it as a loss of ability to grow first, and the loss of current income levels second. Facebook is free, and so advertising is the primary way to make money. There is a strong tension between getting revenue from ads and the quality of the user experience. A lousier user experience means people will migrate to other platforms. As Facebook is going public the pressure will be on to ever-increase revenue, which in turn means more advertisements and in turn means a lousier user experience. It’s a tough circle to play in.

Growth in use of Facebook through our mobile products, where we do not currently display ads, as a substitute for use on personal computers may negatively affect our revenue and financial results;

Quite fixable

Facebook user growth and engagement on mobile devices depend upon effective operation with mobile operating systems, networks, and standards that we do not control;

Apple and Google could make things hard for Facebook on iOS and Android if they so choose, and they may do so.

We may not be successful in our efforts to grow and further monetize the Facebook Platform;

Facebook makes 17% of revenue from clipping the ticket on payments for virtual games. How sustainable is that?

Improper access to or disclosure of our users’ information could harm our reputation and adversely affect our business;

Privacy is still a major concern for Facebook.

Our CEO has control over key decision making as a result of his control of a majority of our voting stock;

I’m actually ok with this, as it hopefully means decisions will be made with respect to usability and long term sustainability rather than quarterly reporting. We shall see.

The loss of Mark Zuckerberg, Sheryl K. Sandberg, or other key personnel could harm our business;

Quite.

Our business is subject to complex and evolving U.S. and foreign laws and regulations regarding privacy, data protection, and other matters. Many of these laws and regulations are subject to change and uncertain interpretation, and could harm our business;

SOPA and other draconian legislation ideas could have a real impact on Facebook. However having Facebook as a large listed company will increase their voice on the Hill.The question is how they will lobby.

We anticipate that we will expend substantial funds in connection with tax withholding and remittance obligations related to the initial settlement of our restricted stock units (RSUs) approximately six months following our initial public offering;

Put that in the valuation models.

The market price of our Class A common stock may be volatile or may decline, and you may not be able to resell your shares at or above the initial public offering price; and

Substantial blocks of our total outstanding shares may be sold into the market as “lock-up” periods end, as further described in “Shares Eligible for Future Sale.” If there are substantial sales of shares of our common stock, the price of our Class A common stock could decline.

This is going to be a rocky ride.

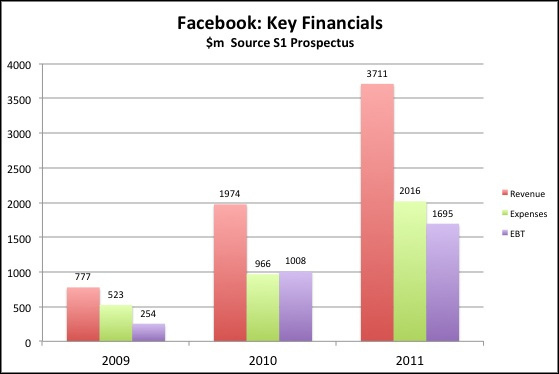

The standard revenue and expenses numbers look like this:

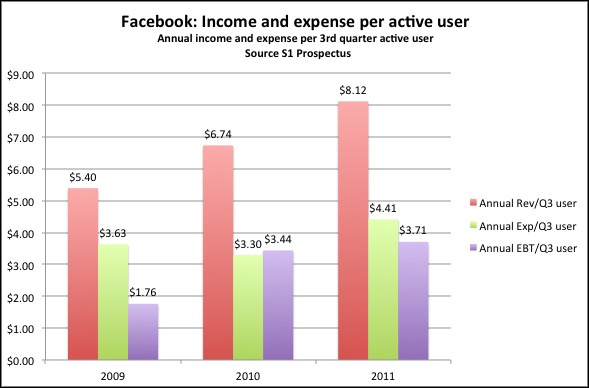

What’s interesting is looking at these on a per user basis. This is difficult to do as I don’t have the quarterly revenue figures to match with the monthly users, and even then we need to really get down to smaller periods so that the number of users is relatively static over the averaging period. In an attempt to get the weighted average I’m going with the end of 3rd quarter numbers of active daily users for this chart. Those users are worth about $8.12 each per annum right now.

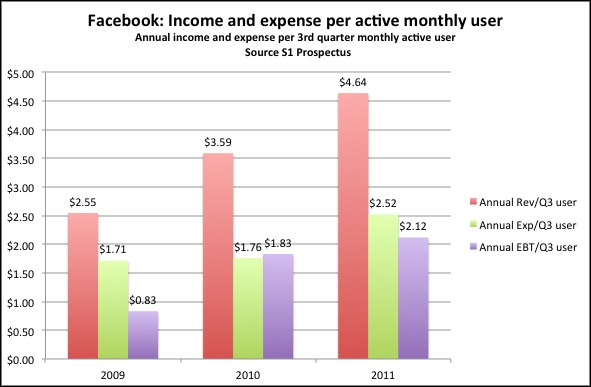

Let’s try the active monthly users chart:

Most users are not active each day, and the average value of each of the people that checks Facebook at least once a month is just $2.12 per year.

Let’s thinking about those numbers in practical terms. As a user Facebook makes money from you if you are exposed (weak) or click (strong) on advertisements and buy things (very strong), or if you partake in the many social games and pay money to the provider through Facebook’s payment system. The question to ask is how often people are clicking on advertisements, and how effective they are. Facebook will be working hard to increase the effectiveness of advertising targeting, and on selling to adland, but ultimately the results are in our hands.

The question to ask as you make a decision to invest or not is simple – how many regular customers will Facebook have, how long will they have them for, and how much money per year will each customer deliver.

At the end of 2011 there were 483 million daily active users, and if we assume 6% growth for each of the next two quarters then 4% growth for the quarters after that then the Dec 31 2012 active daily users will be 587 million. The third quarter number would be 564 million.

At the moment the gross revenue per active user (at the end of the third quarter) is $8.12, a 20% lift on 2010, which was almost 25% up on 2009. Let’s assume growth of 17%, whihc gives a nice round $9.50 per active end 3rd quarter user per year.

That would mean total revenue of 564 million x $9.50 = $5.358 billion for 2012, 44% up on 2011. After that it gets interesting. Will Facebook users actually keep climbing? Will the average revenue per user do the same? How good will Facebook be at controlling expenses, which climbed over 100% from 2010 to 2011?

When it comes to valuing the company, think about the total amount of money that each active user will ever be worth Facebook. If active users were worth $10 each per year, then Facebook would need to keep 1 billion users for 10 years just to earn $100 billion in revenue. Subtract from that the expenses and the considerable time value of money, and we can see a large gulf when looking at hte $100 billion valuation.

However if the average revenue per active user crept up to $25, then 1 billion of them would deliver $125 billion in revenue per year, and an easy $15 billion or so in net. That will take a few year to get to, but justifies a $100 billion value.

So the questions to answer are simple: Can Facebook over double the number of daily active users, and Facebook over triple the dollars that each active user is worth to them each year.

From my own experiences, dropping out of active Facebook participation and using blogging and Twitter only, I see this is very difficult. It seems hard to imagine higher penetration of Facebook in most Western markets, and there are portends of an early adopter migration to elsewhere, including Google +, Twitter or nowhere in particular. The expansion into new markets is also problematic as the average revenue per user will be lower in those lower income per capita areas.

I wish Facebook luck with the IPO, it will be a good one, but I will not be investing.

Entrepreneur and industry commentator Lance Wiggs blogs at LanceWiggs.com.

Further reading: Facebook Files IPO: What It Means For You (ReadWriteWeb)

Sign up to get the latest stories and insights delivered to your inbox – free, every day.

Sign up to get the latest stories and insights delivered to your inbox – free, every day.